Question 111

The following transactions and events occurred during the year:

- $300,000 of raw materials were purchased, of which $20,000 were returned because of defects

- $600,000 of direct labor costs were incurred.

- S750.000 of manufacturing overhead costs were incurred.

What is the organization's cost of goods sold for the year?

- $300,000 of raw materials were purchased, of which $20,000 were returned because of defects

- $600,000 of direct labor costs were incurred.

- S750.000 of manufacturing overhead costs were incurred.

What is the organization's cost of goods sold for the year?

Question 112

Which of the following statements is false regarding roles and responsibilities pertaining to risk management and control?

Question 113

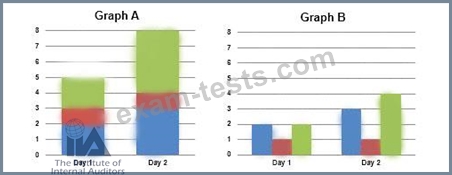

Click the Exhibit.

Internal auditors are asked to keep track of how many hours per day they spend planning the audit, conducting the engagement, and writing the audit report. The data for two days has been collected as follows:

Day 1

Day 2

Planning the audit

2 hours

3 hours

Conducting the engagement

1 hour

1 hour

Writing the audit report

2 hours

4 hours

Which of the following graphs depicts the data accurately?

Internal auditors are asked to keep track of how many hours per day they spend planning the audit, conducting the engagement, and writing the audit report. The data for two days has been collected as follows:

Day 1

Day 2

Planning the audit

2 hours

3 hours

Conducting the engagement

1 hour

1 hour

Writing the audit report

2 hours

4 hours

Which of the following graphs depicts the data accurately?

Question 114

During an audit, the client questions the internal audit activity's authority to perform procedures over fraud allegations. According to HA guidance, which of the following would provide the most relevant support to respond to the client's concerns?

Question 115

When establishing a quality assurance and improvement program, the chief audit executive should ensure the program is designed to accomplish which of the following objectives?

1. Add value.

2. Improve operations.

3. Provide assurance that the internal audit activity conforms with the Standards.

4. Provide assurance that the internal audit activity conforms with the IIA Code of Ethics.

1. Add value.

2. Improve operations.

3. Provide assurance that the internal audit activity conforms with the Standards.

4. Provide assurance that the internal audit activity conforms with the IIA Code of Ethics.