Question 41

What does the deduction method of giving double taxation relief mean?

Question 42

If a parent entity is to be exempt from preparing consolidated financial statements it needs to satisfy certain conditions according to IFRS 10 Consolidated Financial Statements.

Which TWO of the following are conditions that need to be satisfied to be exempt?

Which TWO of the following are conditions that need to be satisfied to be exempt?

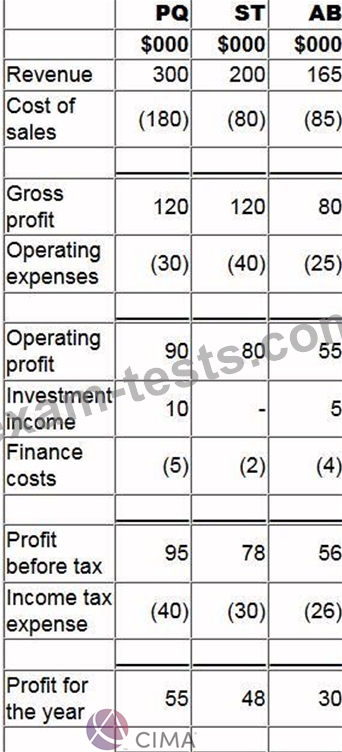

Question 43

The statement of profit or loss for PQ, ST and AB for the year ended 31 December 20X0 are shown below:

1. PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September

20X0.

2. Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3. Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4. PQ uses the fair value method for non-controlling interest at acquisition.

What is the value of the unrealized profit in inventory adjustment required to inventory in PQ's consolidated statement of financial position at 31 December 20X0?

1. PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September

20X0.

2. Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3. Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4. PQ uses the fair value method for non-controlling interest at acquisition.

What is the value of the unrealized profit in inventory adjustment required to inventory in PQ's consolidated statement of financial position at 31 December 20X0?

Question 44

An entity bought a capital item for $110,000 on 1 March 20X4 incurring legal fees at the date of purchase of $2,500.

On 1 May 20X4 additional costs classified as capital expenditure by the tax rules of the country of

$25,000 were incurred in respect of the asset. On 1 June 20X4 repairs not classified as capital expenditure were incurred at a cost of $15,000.

The asset was sold for $250,000 on 30 November 20X8 and costs to sell were incurred of $4,300.

Calculate the chargeable gain on the disposal.

Give your answer to the nearest $.

On 1 May 20X4 additional costs classified as capital expenditure by the tax rules of the country of

$25,000 were incurred in respect of the asset. On 1 June 20X4 repairs not classified as capital expenditure were incurred at a cost of $15,000.

The asset was sold for $250,000 on 30 November 20X8 and costs to sell were incurred of $4,300.

Calculate the chargeable gain on the disposal.

Give your answer to the nearest $.

Question 45

XY purchased a building on 1 April 20X1 for $300,000 with a useful economic life of 30 years. On 1 April

20X7 the building was revalued at $525,000.

What will the new depreciation charge be following the revaluation?

Give your answer as a whole number.

20X7 the building was revalued at $525,000.

What will the new depreciation charge be following the revaluation?

Give your answer as a whole number.